On 13th December 2024, FitchRatings affirmed Tanzania’s Long-Term Foreign-Currency Issuer Default Rating (IDR) at ‘B+’ with a Stable Outlook.

The decision reflects the country’s strong real GDP growth, low inflation, and moderate government debt levels, supported by its ongoing International Monetary Fund (IMF) program.

Economic Growth and Stability

Tanzania’s real GDP growth is projected to accelerate to 5.4% in 2024 and 5.9% in 2025, driven by agriculture, mining, tourism, and infrastructure projects such as the Standard Gauge Railway and the Julius Nyerere Hydropower Project.

Longer-term growth may benefit from the development of offshore gas fields and LNG production. Fitch highlights that while growth volatility is low, reliance on rain-fed agriculture poses risks to economic stability.

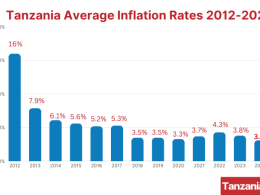

Inflation remains under control, averaging 3.1% in the third quarter of 2024, below the Bank of Tanzania’s 5% target. This is attributed to favorable weather, lower energy costs, and strong foreign exchange inflows.

Fitch forecasts inflation to remain below target at 3.1% in 2024 and 3.4% in 2025, despite potential pre-election spending pressures.

Policy Reforms and Fiscal Management

Reforms under the IMF’s Extended Credit Facility (ECF), extended to May 2026, are bolstering Tanzania’s macroeconomic framework. The Bank of Tanzania’s transition to an interest-rate-based monetary policy framework is a positive step, but structural weaknesses persist, including foreign exchange (FX) pressures and liquidity management challenges. FX reserves are expected to increase to USD 5.6 billion by the end of 2024, equivalent to 3.6 months of current external payments.

Tanzania’s central government debt remains moderate at 48.5% of GDP for the fiscal year 2024, supported by concessional loans constituting 71% of external debt. Fitch projects the debt-to-GDP ratio to decline to 47% by fiscal year 2026.

Challenges and Risks

Revenue underperformance remains a constraint, with non-tax revenue falling short of targets in the first quarter of fiscal year 2025.

Fitch forecasts a budget deficit of 3.4% of GDP for fiscal year 2025, higher than the government’s projection of 2.9%.

Interest costs are rising, with the central government’s interest-to-revenue ratio expected to exceed 16% in fiscal year 2025, driven by higher debt costs.

Fitch notes progress in public financial management, including efforts to reduce domestic arrears, which have fallen to 0.6% of GDP as of September 2024. However, political tensions ahead of the October 2025 general election may pose risks to policy continuity. While recent local elections saw the ruling party secure a decisive victory, increased arrests of opposition members have heightened tensions.

Key Drivers for Future Rating Changes

Fitch outlined several factors that could influence future rating adjustments:

- Negative Rating Action: Persistent current account deficits, foreign exchange reserve depletion, or weakening macroeconomic stability.

- Positive Rating Action: Improved revenue mobilization, sustained fiscal consolidation, and enhanced confidence in exchange rate and FX intervention frameworks.

ESG Considerations

Tanzania’s governance and institutional quality remain critical factors in its rating, with medium rankings in the World Bank Governance Indicators. Issues such as corruption and limited institutional capacity weigh on the credit profile, despite recent improvements.